{kind=link}

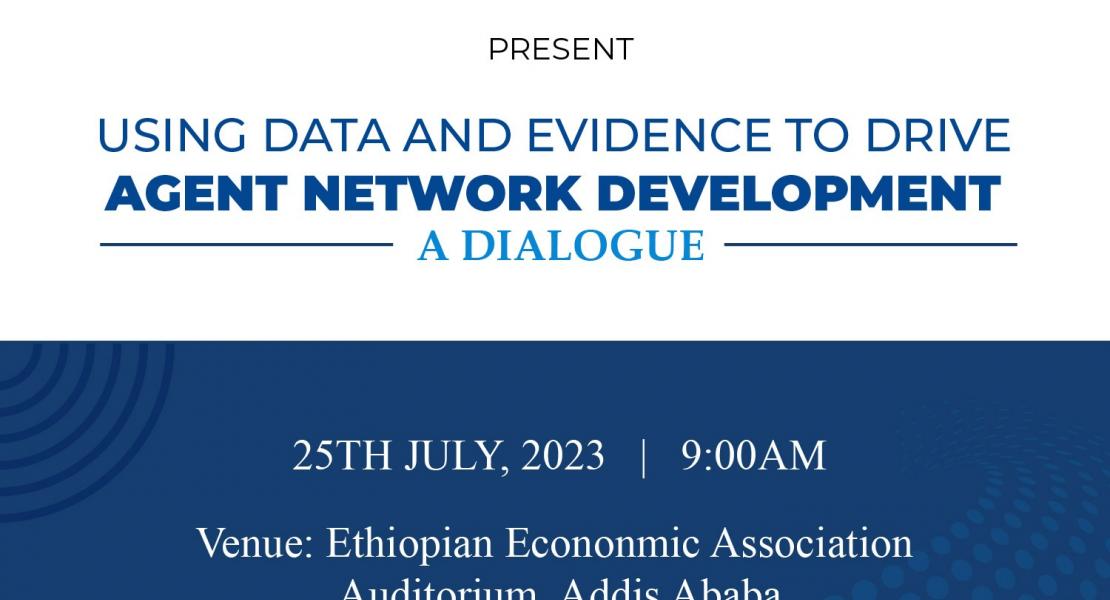

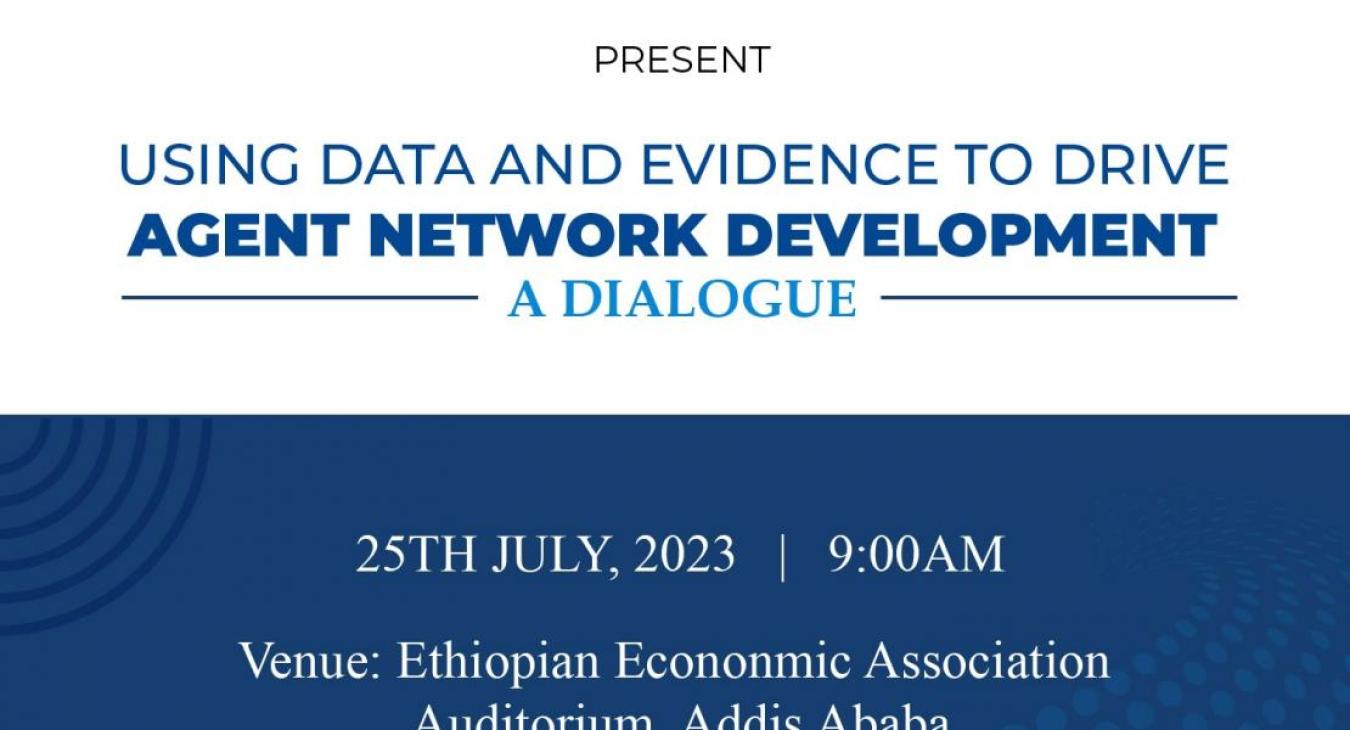

The Retail Finance Development Research Initiative (ReFinD) and the United Nations Capital Development Fund (UNCDF) are joining forces to co-host a dialogue centered on leveraging data to drive the development of agent networks. The event, scheduled for July 25, 2023, is part of this year's Evidence to Action Conference taking place in Addis Ababa, Ethiopia.

Under the theme "Driving Financial Resilience at the Last Mile – Lessons in Evidence-led Agent Network Development," the dialogue aims to convene researchers, policymakers, commercial providers of agent networks, financial service providers, and development practitioners. Together, they will delve into existing interventions and explore the generation and integration of evidence for agent network development in remote areas. The dialogue will also serve as a platform for Ethiopia's agent network ecosystem to interact and review industry best practices regarding evidence integration.

The keynote address will be delivered by Temesgan Zeleke, Director of the Financial Inclusion Secretariat at the National Bank of Ethiopia. Additionally, Professor Peter Quartey, Executive Director of ReFinD, will present on evidence integration in agent network development in low-income countries. The event will feature a panel discussion featuring esteemed experts from the field.

Prof. Quartey, who is also the Director of ISSER, expressed enthusiasm about the upcoming dialogue, stating, "We are delighted to be active participants in this year’s Evidence to Action Conference and hope that this joint event with UNCDF will foster meaningful exchanges and deepen our understanding of the role of evidence in promoting agent networks as a tool for financial resilience.”

The dialogue will take place at the main auditorium of the Ethiopian Economic Association (EEA) in Yeka Sub City, Woreda 11 CMC, Kebele 19.

To reserve a seat in advance, please contact the ReFinD team via email at refind.isser@ug.edu.gh or by phone at +233 244 766 492.