{kind=link}

An informal enterprise operator shares insights during ISSER-led training, part of a study exploring how entrepreneurs can deliver digitised microinsurance services and expand agent networks in Ghana.

By Edem Klobodu

Walk through any neighborhood in Accra, and you will spot small kiosks draped in colorful MTN, Vodafone, or Telecel branding operated by entrepreneurs who keep Ghana’s digital economy humming. These mobile money agents process billions of cedis in transactions annually, serving as de facto banks for millions without access to traditional financial services. But here’s what you won’t see from the street: nearly half of these agents are silently wrestling with common mental disorders.

The numbers behind the counter

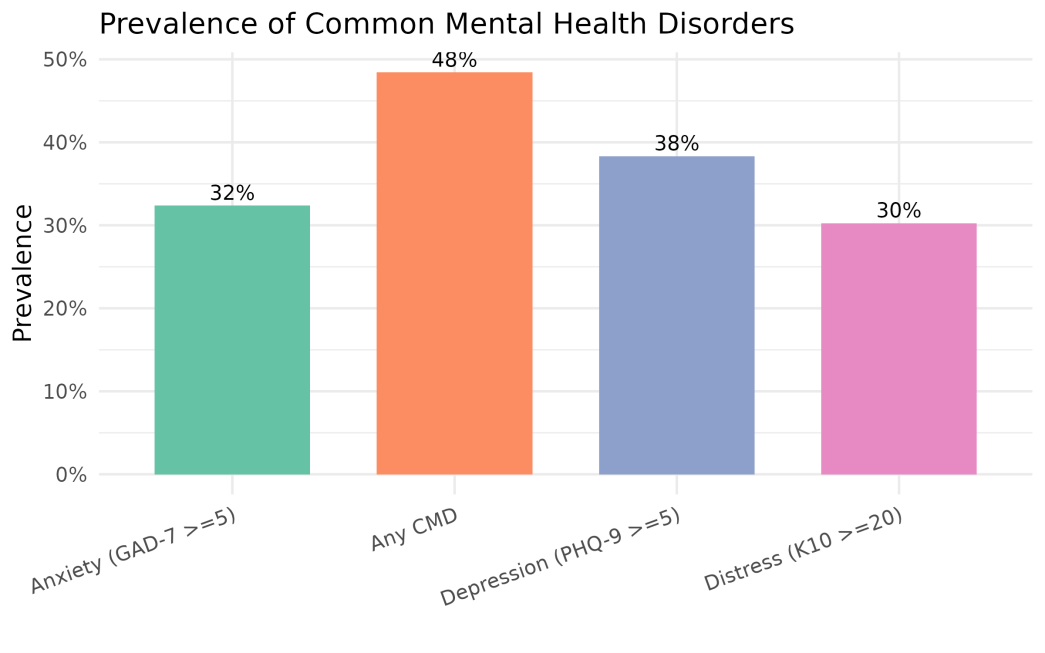

From June to July 2025, we surveyed over 800 mobile money agents across Greater Accra using clinically validated screening tools. The results were sobering: 48% met screening thresholds for at least one common mental disorder: 38% for depression, 32% for anxiety, and 30% for high psychological distress.

Figure 1: Prevalence of Common Mental Disorders (CMD) among Mobile Money Agents

These rates exceed Ghana’s general population, where depression prevalence is approximately 25% (Amu et al., 2021). But perhaps more striking was what agents didn’t do: they didn’t stay home.

The hidden costs nobody talks about

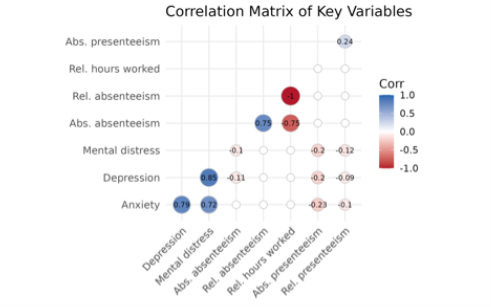

Most agents are self-employed or work on commission, where no work means no income. So they show up every day, even when struggling. This phenomenon, known as presenteeism, creates a different cost. Agents with higher distress scores showed lower on-the-job performance: more errors, slower service, and reduced ability to handle difficult customers.

Figure 2: Mental Health and Productivity Correlations

We also found that about 30% of agents spend significant sums on painkillers, energy drinks, and herbal remedies just to get through the workday -- survival tactics rather than health investments.

What’s driving the distress?

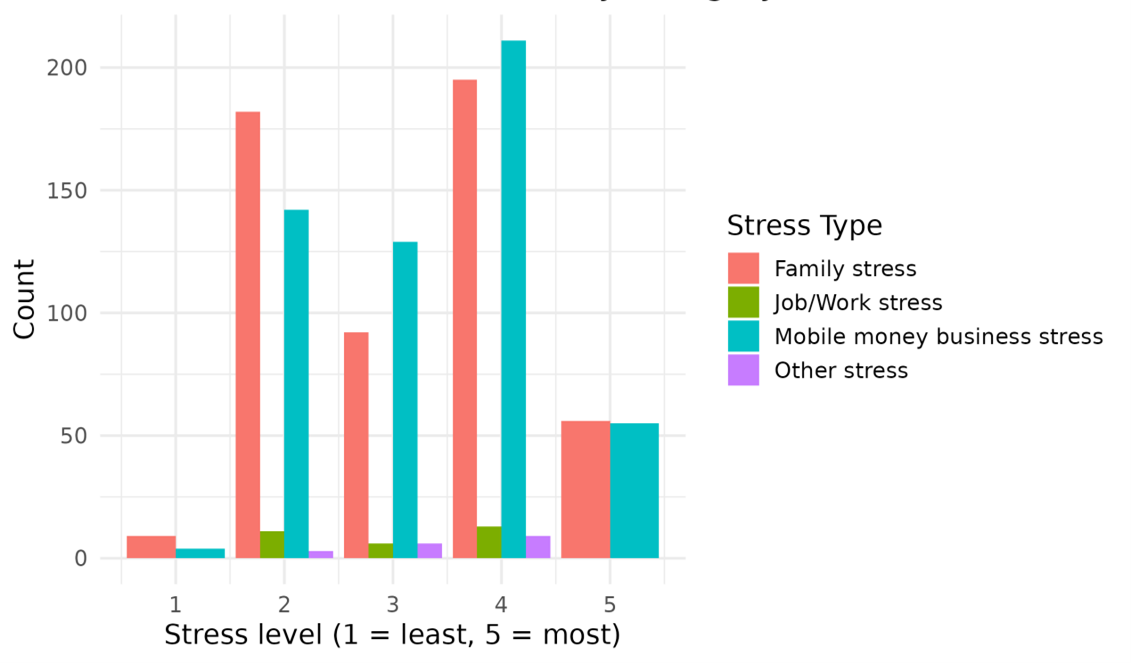

When agents rated stress across life domains, mobile money business stress dominated; most rated it 4 or 5 on a 5-point scale. The reasons are clear: constant liquidity pressures, fraud risks, customer conflicts, and long hours with little time for recovery. Agents operating mobile money only reported higher distress than those with diversified businesses, suggesting income diversification may buffer against stress.

Figure 3: Distribution of Stress Scores by Category

Many agents told us this was the first time anyone asked about their well-being.

What comes next

We are now preparing a pilot study to test whether targeted psychological and financial support can help. If effective, the implications extend far beyond Ghana. Agent-based models are the backbone of digital financial services across Africa.

The takeaway for telecoms, regulators, and fintech actors is this -- mobile money’s success rests on agent networks, yet the current model extracts value from agents without adequately supporting them. Investing in agent well-being is not just an ethical imperative, it is essential for the long-term sustainability of mobile money services. The hidden costs of distress ultimately undermine service quality and network stability.

For now, the message is simple: The people powering Africa’s fintech revolution are struggling, and we can no longer afford to look away.

Edem Klobodu is an assistant professor of marketing at the Smith School of Business, Queen’s University. This research is supported by the Retail Finance Distribution (ReFinD) Research Initiative and conducted in partnership with Telecel Ghana.